The Intelligent Investor marks a significant deviation to stock selection from the earlier works of Benjamin Graham, Warren Buffett's mentor.

Interviews (Unverifiable)

1. An Hour with Mr. Graham (1976)

In a 1976 interview, Graham supposedly explains the shift in paradigm as:

"The thing that I have been emphasizing in my own work for the last few years has been the group approach. To try to buy groups of stocks that meet some simple criterion for being undervalued-regardless of the industry and with very little attention to the individual company"

"I found the results were very good for 50 years. They certainly did twice as well as the Dow Jones. And so my enthusiasm has been transferred from the selective to the group approach."

2. A Conversation with Benjamin Graham (1976)

In a different 1976 interview, Graham allegedly says:

"I am no longer an advocate of elaborate techniques of security analysis in order to find superior value opportunities. This was a rewarding activity, say, 40 years ago, when our textbook "Graham and Dodd" was first published; but the situation has changed a great deal since then. In the old days any well-trained security analyst could do a good professional job of selecting undervalued issues through detailed studies; but in the light of the enormous amount of research now being carried on, I doubt whether in most cases such extensive efforts will generate sufficiently superior selections to justify their cost. To that very limited extent I'm on the side of the "efficient market" school of thought now generally accepted by the professors."

Efficient Market Hypothesis

Please note the qualifier that Graham allegedly used above - "To that very limited extent". The statement does not in any way mean that Graham believed in the Efficient Market Hypothesis (EMH).

Graham also supposedly explains why inefficiencies exist — because a lot of really good stocks are neglected.

"The typical investor has a great advantage over the large institutions."

"Chiefly because these institutions have a relatively small field of common stocks to choose from--say 300 to 400 huge corporations--and they are constrained more or less to concentrate their research and decisions on this much over-analyzed group. By contrast, most individuals can choose at any time among some 3000 issues listed in the Standard & Poor's Monthly Stock Guide."

Group Approaches

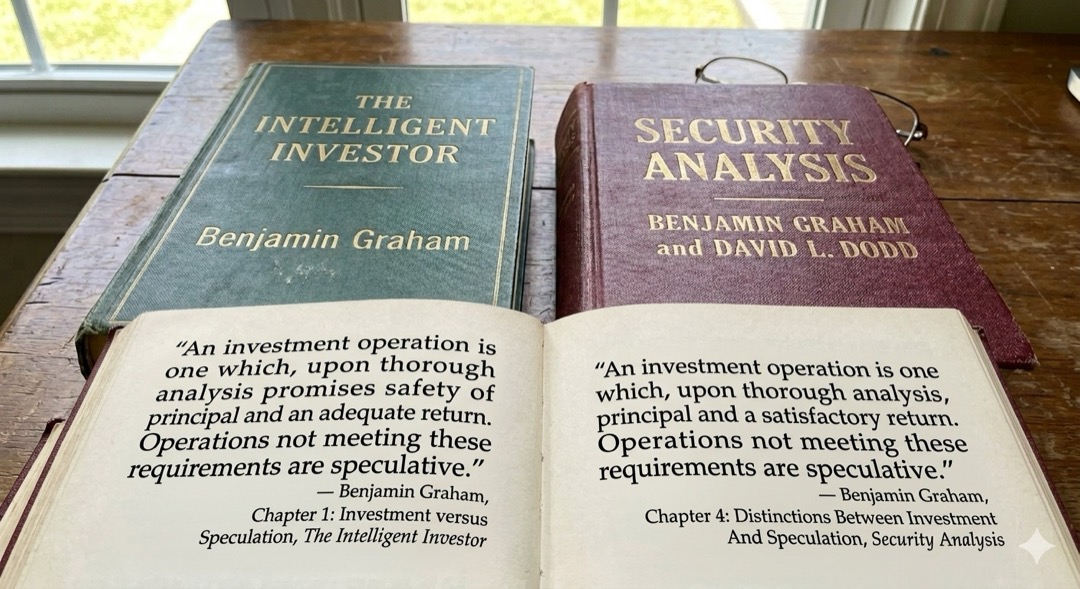

What Graham may have been referring to here is the shift in paradigm from his earlier book Security Analysis (credited to Graham and his assisting student David Dodd), to his later work in The Intelligent Investor (authored by Graham alone).

The Intelligent Investor marks a significant deviation to stock selection from Graham's earlier works; with specific broad techniques now being recorded and discussed, instead of detailed analyses of single stocks.

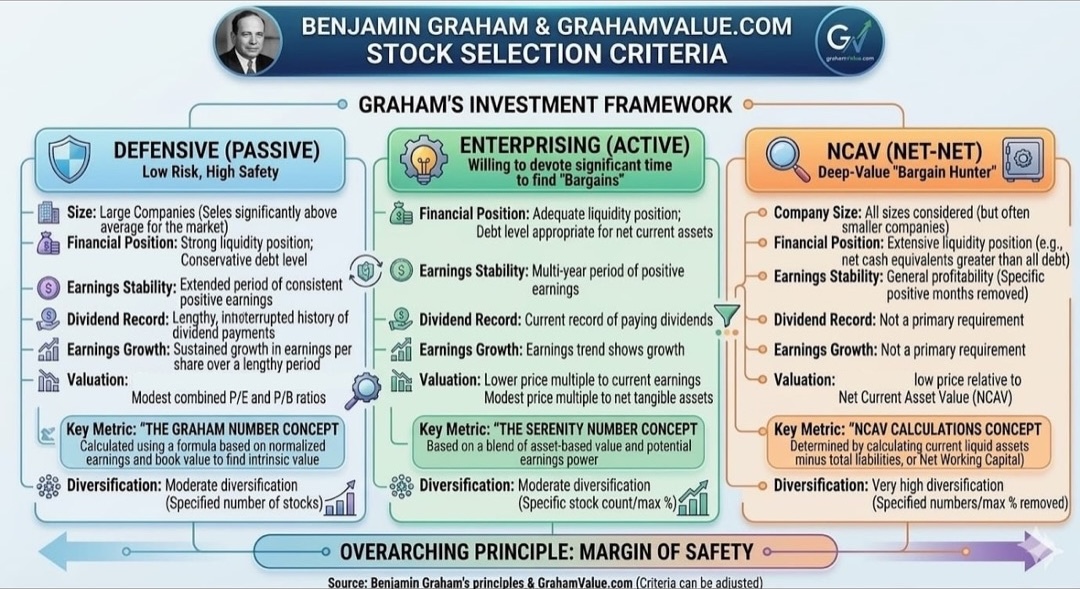

Group approaches such as NCAV are now covered in detail in The Intelligent Investor.

The Intelligent Investor (Verifiable)

Please note that neither of the primary sources for the above interviews are verifiable, and secondary Value Investing sources are often replete with misquotes.

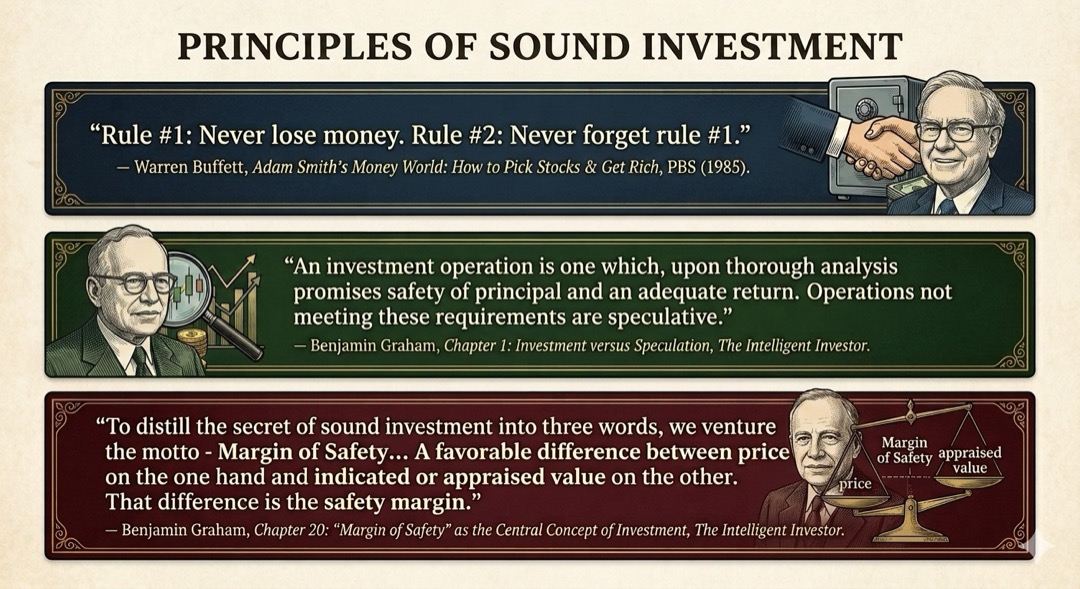

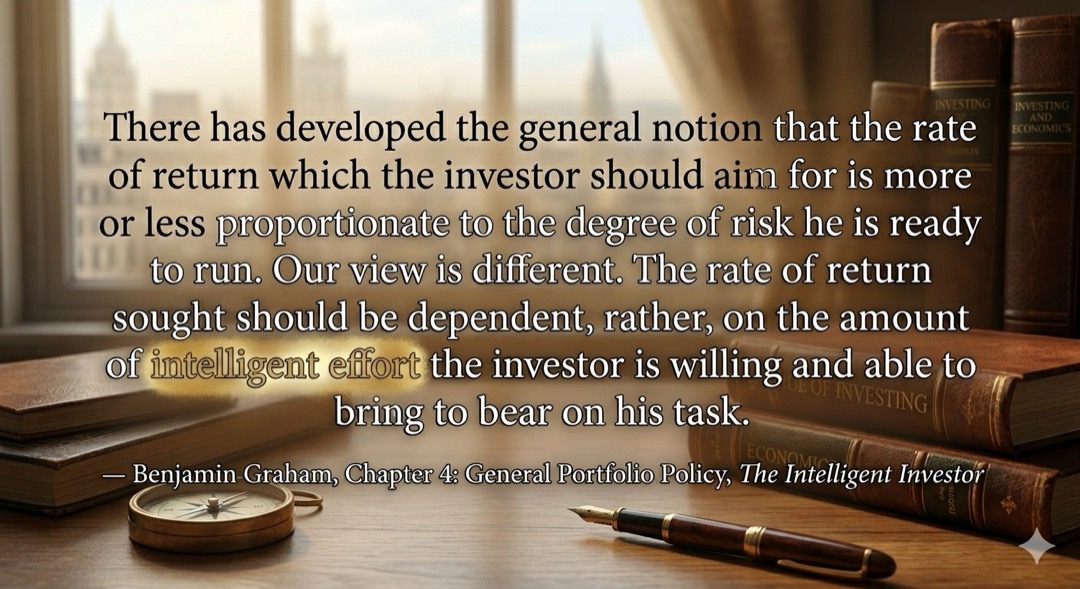

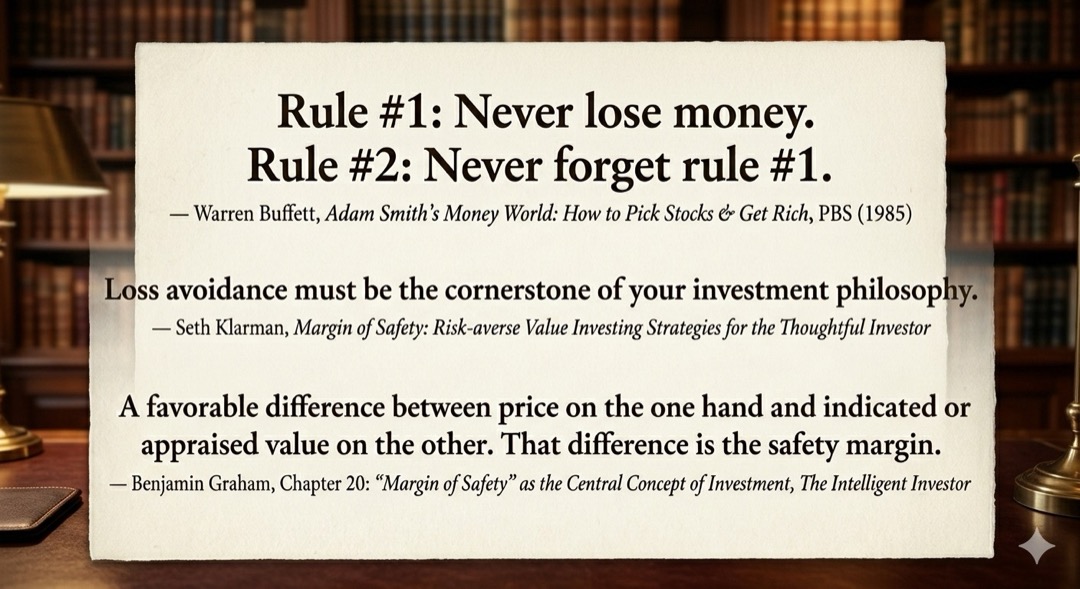

But Graham wrote the last edition of The Intelligent Investor in 1973, just three years before his passing. Value Investors such as Buffett and Klarmam have continued to swear by Graham's methods; even as recently as 2018.

"In 1949, The Intelligent Investor was published. This was a book for the layman but it focused on security analysis and gave prestige to the field. "

Security Analysis has entire chapters dedicated to specific selection criteria for Bonds.

But while Graham does go into great detail about stocks in Security Analysis, he does not give specific instructions on actual application.

The Intelligent Investor, however, was written almost twenty years after the first edition of Security Analysis.

Both books go into great detail on why Value beats Growth and other approaches to other investing.

They also address all the usual instinctive reactions and criticisms of Value Investing. Both books address all other aspects of investing such as Bonds, Warrants and Preferred Stocks in great detail as well.

But only The Intelligent Investor has specific rules and entire chapters dedicated to the subject of stock selection.

Applies Security Analysis

Chapter 14: Stock Selection for the Defensive Investor starts with the line "It is time to turn to some broader applications of the techniques of security analysis".

The Intelligent Investor is the intellectual successor Graham's earlier work, Security Analysis, and gives specific techniques of application; as well as detailed explanations of the reasoning behind each of them. These explanations address all common questions and criticisms of Value Investing, and form the major portion of the eighteen chapters apart from the ones on stock selection.

Discusses Single Criteria

Chapter 15: Stock Selection for the Enterprising Investor has a section specifically titled "Single Criteria for Choosing Common Stocks".

"We have already pointed out that the low-multiplier criterion applied to the DJIA at the end of 1968 worked out badly when the results are measured to mid-1971. The record of common-stock purchases made at a price below their working-capital value has no such bad mark against it."

"We have made a series of “experiments,” each based on a single, fairly obvious criterion... To that extent the results support our recommendation that the issues selected meet a combination of quantitative or tangible criteria."

GrahamValue's analyses and stock screeners strictly follow Graham's group selection rules (including NCAV) as given in The Intelligent Investor.

Buffett about Graham

Named son after him

Warren Buffett talks about his working and personal relationship with Graham, naming his son after Graham, the time he offered to work for Graham for free, and how — contrary to a common misconception today — Graham was uninfluenced by the Great Depression.

Methods that work for anyone

Buffett explains how Graham didn't want to do anything that a reader of his book couldn't do; and Munger explains that Graham was "a truly formidable mind", but was looking for methods that would work for anyone.

On other occasions, Buffett has also explained that meeting managements etc is only required when buying the whole business.

Hi-Res Quotes and Images

Note: Click on the chevron (‹ and ›) or button (○) symbols to scroll through the image carousel below.

Submitted by GrahamValue. Created on Thursday 25th June 2015. Updated on Thursday 6th July 2023.