The wisest and wittiest quotes by Value Investing legend Warren Buffett; and a curated list of quotes by his mentor, Benjamin Graham.

Buffett and Graham

Benjamin Graham was a scholar and professional investor who mentored some of the world's most renowned investors; including Warren Buffett, Sir John Templeton, Bill Ruane, Irving Kahn and Walter Schloss.

"Rule #1: Never lose money. Rule #2: Never forget rule #1."

"In the old legend the wise men finally boiled down the history of mortal affairs into the single phrase, "This too will pass." Confronted with a like challenge to distill the secret of sound investment into three words, we venture the motto - Margin of Safety."

Quotes

Many of the quotes attributed today to Graham, are actually from the commentary by Jason Zweig in recent editions of The Intelligent Investor. Given below are a selection of quotes by Buffett, as well as a list of quotes by Benjamin Graham from his books and interviews.

By Warren Buffett

"Price is what you pay. Value is what you get."

"Time is the friend of the wonderful company, the enemy of the mediocre."

"In the business world, the rear-view mirror is always clearer than the windshield."

"There seems to be some perverse human characteristic that likes to make easy things difficult."

"It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price."

"Never ask a barber if you need a haircut."

"As a group, lemmings have a rotten image, but no individual lemming has ever received bad press."

"Wall Street is the only place that people drive to in a Rolls Royce to take advice from people who ride the subway."

"Beware of geeks bearing formulas."

"Only when you combine sound intellect with emotional discipline do you get rational behavior."

"The business schools reward difficult complex behavior more than simple behavior, but simple behavior is more effective."

"Unless you can watch your stock holding decline by 50% without becoming panic-stricken, you should not be in the stock market."

"Never invest in a business you can’t understand."

"Risk comes from not knowing what you're doing."

"Risk can be greatly reduced by concentrating on only a few holdings."

"Wide diversification is only required when investors do not understand what they are doing."

"Stop trying to predict the direction of the stock market, the economy, interest rates, or elections."

"Remember that the stock market is manic-depressive."

"Only when the tide goes out do you discover who's been swimming naked."

"Be fearful when others are greedy and greedy only when others are fearful."

"When you combine ignorance and leverage, you get some pretty interesting results."

"Our favorite holding period is forever."

"The rich invest in time, the poor invest in money."

"As far as you are concerned, the stock market does not exist. Ignore it."

"Much success can be attributed to inactivity. Most investors cannot resist the temptation to constantly buy and sell."

"Lethargy, bordering on sloth should remain the cornerstone of an investment style."

"The most important thing to do if you find yourself in a hole is to stop digging."

"You only have to do a very few things right in your life so long as you don't do too many things wrong."

"It takes 20 years to build a reputation and five minutes to ruin it. If you think about that, you'll do things differently."

"The difference between successful people and really successful people is that really successful people say no to almost everything."

"I never attempt to make money on the stock market. I buy on assumption they could close the market the next day and not re-open it for five years."

"No matter how great the talent or efforts, some things just take time. You can't produce a baby in one month by getting nine women pregnant."

"Focus on return on equity, not earnings per share."

"Do not take yearly results too seriously. Instead, focus on four or five-year averages."

"If you've been playing poker for half an hour and you still don't know who the patsy is, you're the patsy."

"Should you find yourself in a chronically leaking boat, energy devoted to changing vessels is likely to be more productive than energy devoted to patching leaks."

"Investors should remember that their scorecard is not computed using Olympic-diving methods: Degree-of-difficulty doesn't count."

"It is extraordinary to me that the idea of buying dollar bills for 40 cents takes immediately with people or it doesn't take at all. It's like an inoculation. If it doesn't grab a person right away, I find you can talk to him for years and show him records, and it doesn't make any difference."

"Most analysts feel they must choose between two approaches customarily thought to be in opposition:"value" and"growth." In our opinion, the two approaches are joined at the hip: Growth is always a component in the calculation of value, constituting a variable whose importance can range from negligible to enormous and whose impact can be negative as well as positive."

By Benjamin Graham

“Though business conditions may change, corporations and securities may change, and financial institutions and regulations may change, human nature remains the same. Thus the important and difficult part of sound investment, which hinges upon the investor’s own temperament and attitude, is not much affected by the passing years.”

(From the Introduction to the 1949 edition of The Intelligent Investor, and not present in recent editions)"An investment operation is one which, upon thorough analysis promises safety of principal and an adequate return. Operations not meeting these requirements are speculative."

"While enthusiasm may be necessary for great accomplishments elsewhere, on Wall Street it almost invariably leads to disaster."

"To achieve satisfactory investment results is easier than most people realize; to achieve superior results is harder than it looks."

"In the short run, the market is a voting machine but in the long run, it is a weighing machine."

"there has developed the general notion that the rate of return which the investor should aim for is more or less proportionate to the degree of risk he is ready to run. Our view is different. The rate of return sought should be dependent, rather, on the amount of intelligent effort the investor is willing and able to bring to bear on his task."

"If the reason people invest is to make money, then in seeking advice they are asking others to tell them how to make money. That idea has some element of naïveté."

"Objective tests of managerial ability are few and far from scientific."

"Some matters of vital significance, e.g., the determination of the future prospects of an enterprise, have received little space, because little of definite value can be said on the subject."

"Analysis is concerned primarily with values which are supported by the facts and not with those which depend largely upon expectations."

"In our own stock-market experience and observation, extending over 50 years, we have not known a single person who has consistently or lastingly made money by thus following the market. We do not hesitate to declare that this approach is as fallacious as it is popular."

"The underlying principles of sound investment should not alter from decade to decade, but the application of these principles must be adapted to significant changes in the financial mechanisms and climate."

"With every new wave of optimism or pessimism, we are ready to abandon history and time-tested principles, but we cling tenaciously and unquestioningly to our prejudices."

"Investment is most intelligent when it is most businesslike."

"Operations for profit should be based not on optimism but on arithmetic."

"You are neither right nor wrong because the crowd disagrees with you. You are right because your data and reasoning are right."

"In the world of securities, courage becomes the supreme virtue after adequate knowledge and a tested judgment are at hand."

"Obvious prospects for physical growth in a business do not translate into obvious profits for investors."

"Individuals who cannot master their emotions are ill-suited to profit from the investment process."

"If you are shopping for common stocks, choose them the way you would buy groceries, not the way you would buy perfume."

"The price [of a security] is frequently an essential element, so that a stock may have investment merit at one price level but not at another."

"Obviously it requires strength of character in order to think and to act in opposite fashion from the crowd and also patience to wait for opportunities that may be spaced years apart."

From Graham's books

“All things excellent are as difficult as they are rare.”

"Medius tutissimus ibis (You will go safest in the middle course)."

“They will fluctuate.”

“Buy cheap and sell dear.”

"Many shall be restored that now are fallen and many shall fall that now are in honor."

"Those who do not remember the past are condemned to repeat it."

"Through chances various, through all vicissitudes, we make our way..."

Buffett on Graham

"There will continue to be wide discrepancies between price and value in the marketplace, and those who read their Graham & Dodd will continue to prosper."

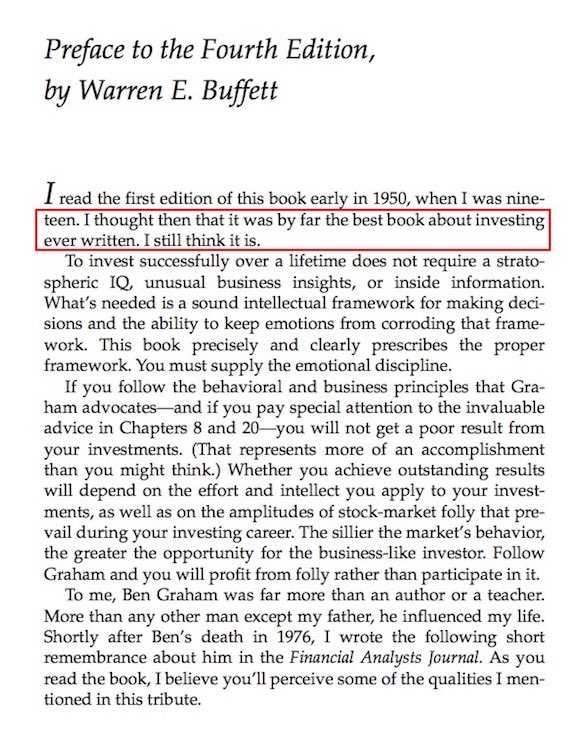

"By far the best book about investing ever written... To invest successfully over a lifetime does not require a stratospheric IQ, unusual business insights, or inside information. What’s needed is a sound intellectual framework for making decisions and the ability to keep emotions from corroding that framework. This book precisely and clearly prescribes the proper framework."

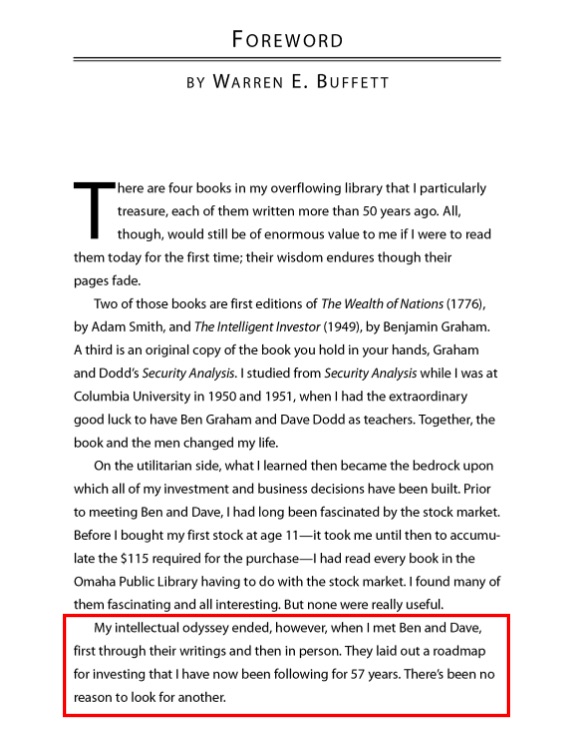

"My intellectual odyssey ended, however, when I met Ben and Dave, first through their writings and then in person. They laid out a roadmap for investing that I have now been following for 57 years. There’s been no reason to look for another."

Others about Graham

"I took Ben’s course in Advanced Security Analysis at the New York Stock Exchange Institute (New York Institute of Finance)... Many bright Wall Streeters such as Gus Levy of Goldman Sachs, who later became the top arbitrageur in the country, used to take his course. I often wondered how much money people made on Ben’s ideas by transforming them into investments."

"Heed the words of the great pioneer of stock analysis Benjamin Graham: 'Buy when most people...including experts...are pessimistic, and sell when they are actively optimistic'."

"[Graham] is the genius who literally created the framework for investment analysis that leads to successful investing. Like that other genius Edison, Graham created light where there was none."

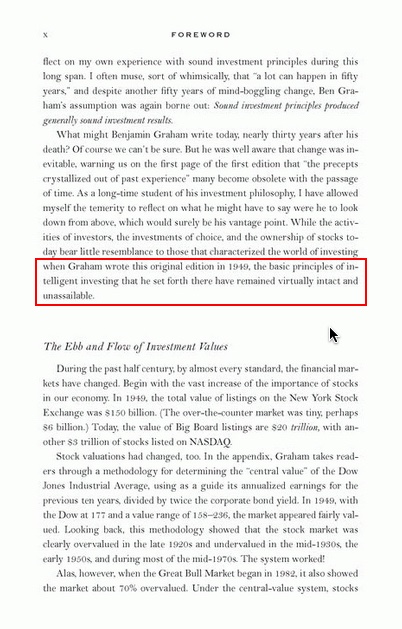

"The basic principles of intelligent investing that [Graham] set forth... have remained virtually intact and unassailable."

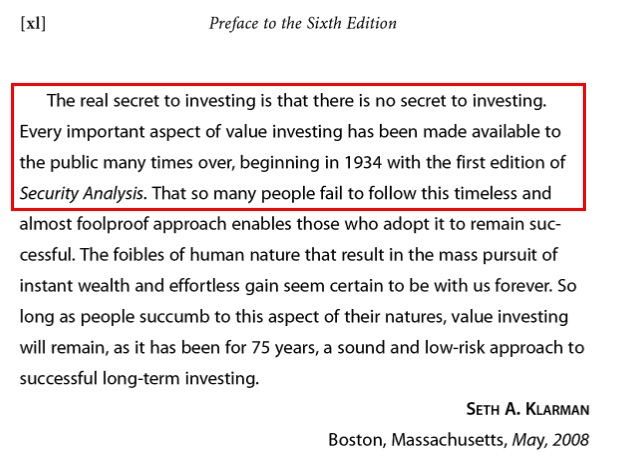

"The real secret to investing is that there is no secret to investing. Every important aspect of value investing has been made available to the public many times over, beginning in 1934 with the first edition of Security Analysis."

"You stick to value, to Benjamin Graham, the man who wrote the bible for the market. It’s a mistake to believe you can do more."

See videos and explanations of the Margin of Safety by Buffett and others.

Watch Videos

Greatest Investing Lessons Of All Time

Benjamin Graham Real Quotes

Facebook Likes and Comments

Warren Buffett, Foreword (2008): Security Analysis (by Benjamin Graham)

Warren Buffett, Preface (1986): The Intelligent Investor (by Benjamin Graham)

Seth Klarman, Preface (2008): Security Analysis (by Benjamin Graham)

John Bogle, Foreword (2005): The Intelligent Investor (by Benjamin Graham)

Irving Kahn, Bloomberg Business: How to Play the Market (2012)

Submitted by GrahamValue. Created on Monday 19th December 2016. Updated on Friday 17th April 2026.